A note for the nerds

a comparison of financial planning methods and my planning philosophy

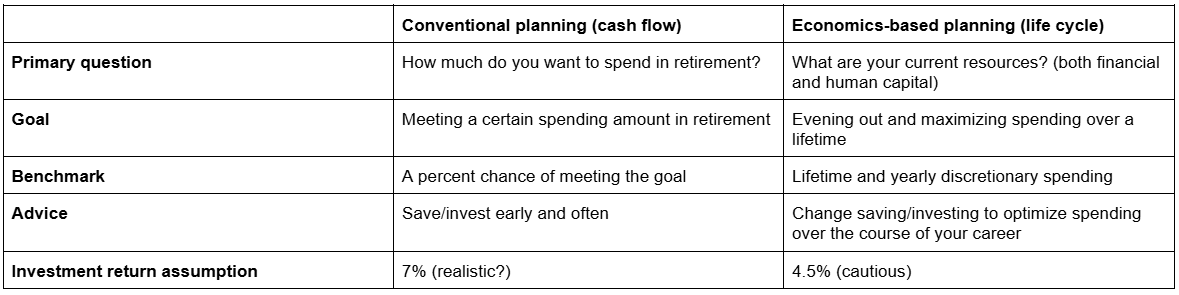

Every piece of financial planning software, every class I’ve taken, and every calculator from Fidelity to Right Capital frames financial planning around a successful retirement. And by successful, they mean hitting a certain spending target.

It looks something like this:

How much do you want to spend in retirement?

How about $6000/month?

Ok. You have a 10% probability of success. Also, you’re not on track to fund your goal of sending your children to college.

If you contribute more to your IRA and retire two years later, we can give you a 31% probability of success.

Even as a financial professional, I find this confusing. I have no freaking clue what I want or need to spend in retirement. What am I supposed to do with this probability of success?? It doesn’t tell me how bad my failure is; it doesn’t account for adjustments to spending over time, nor does it give me clear action today (except maybe indicate that I need to change something). Even if I tinker and adjust, adding more investments, more time working, and less spending, there isn’t a set percentage that I need to reach.

I don’t think I’m alone in this confusion. You want a plan for your finances that is understandable, actionable, and relevant to your life right now. You want to know how much you can spend and how much you should save/invest for your goals. You’ve probably never heard of a Monte Carlo simulation (the model behind those percentages) and have no reference point for what an 82% vs 31% chance of success might mean (except that 82% sounds a lot better). You might have difficulty feeling motivated by a ‘successful retirement’ decades in the future. Yet, this is how 99% of financial planning is done, and part of me feels wholly unqualified (a little imposter syndrome creeping in here) to go against the grain.

As someone who has spent a little too much time in academia, though, I feel like this is all too familiar. Researchers and scientists have a wealth of knowledge and have even developed methods to apply that knowledge into practice - yet they are up against an industry with differing goals and many more resources.

The tools created by the FinTech industry are beautiful. They feel like you’d expect a professional tool to feel. They have progressive disclosure of information and lots and lots of visuals. They allow you to sync your accounts and let your financial professional see the asset allocation and totals in those accounts securely. Almost nothing needs to be done manually. They have a lot of things built into one. But at the end of the day, their method (conventional financial planning or cash flow-based planning) and their output (the percent success) miss the mark.

Enter economics-based planning

Reading Money Magic and the work of

and , I stumbled on another option, an option that <1% of financial advisors use - economics-based planning. As I’ve read more academic research on personal finance and household financial planning and become more versed in traditional planning methods, this option makes more and more sense.At first, economics-based planning seemed a bit counterintuitive. Doing our own financial plan, this method recommended that we spend our savings. CRAZY at first glance but absolutely logical when I took a step back (I mean, what are savings for??). We’re making the lowest amount now than we will probably ever make. A little more savings in a few years when we don’t have kids in daycare and my husband is done with training won’t mean as much as that little bit does now. Now is not the time to save.

To reach that conclusion, the economics-based approach started by asking me how much we make and expect to make (human capital) instead of asking what I want to spend in retirement. It then asked how much I wanted to keep on reserve (an emergency fund). From that, it gave me an amount of money we could safely spend this year at baseline.

or $5,615/month.

Now, that is something concrete I (and I’d like to think you) can work with. We know dollars and cents. We know what $5,615 dollars looks like in our budgets.

To summarize the difference between the two approaches, I made this lovely table:

My planning philosophy.

I’m not so sure about the conventional, cash-flow financial planning method. It has some of the elements of an understandable, actionable, and relevant financial plan but lacks too many of them.

Elements of a good financial plan

A clear spending/savings recommendation based on the resources you have and expect to have.

A timeline and plan to pay for the big things (wedding, kids' college fund, retirement, long-term care, etc.) that balances today with tomorrow.

Room for flexibility. There is a tradeoff here, but we never know what life will throw at us. There are multiple ways to build in flexibility (cautious predictions, an emergency fund, etc.)

Updated information. You don’t need to look at your financial plan every day, but you should update it yearly. The market changes. Tax law changes. Your life changes.

Beyond that, a good financial plan should include:

a plan for what accounts to utilize and when

investment options & their risk/return

the impact of different insurance amounts

tax minimization strategies

maximization of social security and other government programs

estate planning considerations

There isn’t a perfect solution or one piece of software that does everything. However, at baseline, economics-based financial planning starts with a framework that solves the equation for how to best meet your goals today and tomorrow, resulting in a dollar amount to spend and save. Traditional planning asks you (or your financial professional) to decide how much to spend, save, and invest based on a chance of meeting a somewhat arbitrary goal. I know which one I’d rather have.

Also a nerd? Got something to add? I would love to learn what you think.

You have to optimize for the present and the future! That's the idea behind consumption smoothing. You can always set goals, but the baseline assumption and goal is not just one end number. It does make the modeling a little more complicated 😅

You are taking your readers to the state of the art! Well done.